Real estate decisions get easier when you evaluate them through a clear framework instead of guessing where the economy is headed.

1. Rising Sales Show the Market Is Loosening Up

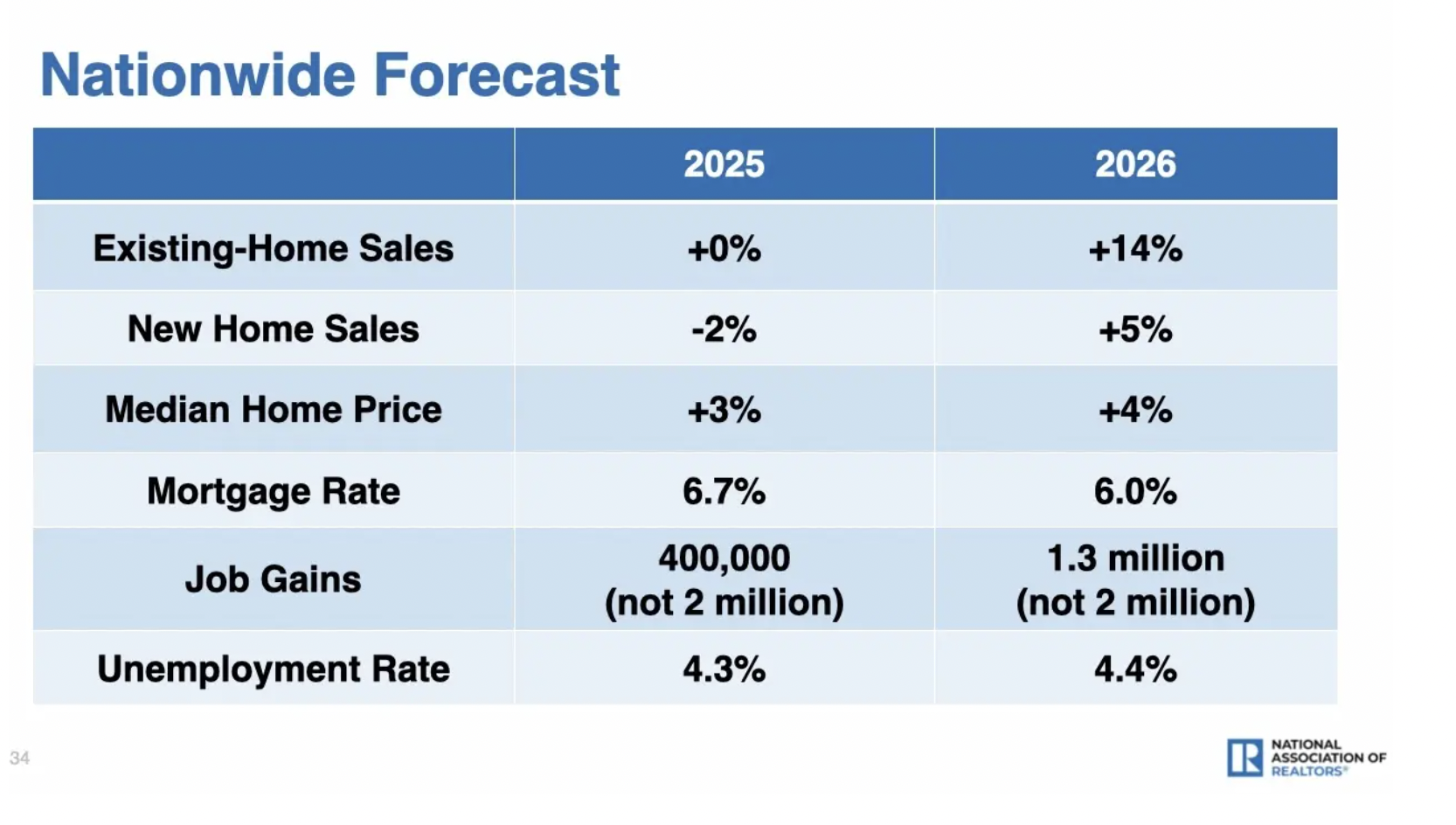

A 14% jump in existing-home sales means buyers finally have more room to move.

After three flat years near 4 million annual sales, an additional 560,000 transactions signals renewed confidence and mobility. For buyers who’ve been waiting out the tightness, this kind of shift opens real opportunity.

More activity means more choices.

The return of movement is a sign to prepare, not pause.

2. Steady Price Growth Creates Healthy, Sustainable Wealth

NAR projects home prices rising 4% in 2026—a pace that builds equity without crushing affordability.

This isn’t the runaway pricing of 2021, nor the stagnation we’ve seen lately. It’s long-term, dependable appreciation—the kind that quietly builds wealth for everyday homeowners.

This is stability, not speculation.

Slow, steady growth is the backbone of real estate wealth.

3. Lower Rates Reopen Both Purchase and Refi Options

With 30-year rates expected near 6%, millions of homeowners regain access to meaningful refinance savings.

ICE estimates roughly 5 million refi candidates at this level—plus added purchase power for buyers who lost ground during the rate spike. And with the labor market cooling, rates could drift even lower.

When money gets cheaper, opportunity expands.

Falling rates are a green light to explore options early.

4. Economic Softening Is Creating the Conditions for Better Deals

Job losses, rising unemployment, and softer labor demand typically pull mortgage rates down.

ADP’s recent data, escalating WARN notices, and higher claims all point toward cooling. For buyers and owners, that cooling often translates into more favorable financing and better negotiating leverage.

Soft labor equals softer money.

Economic cooling is uncomfortable, but it creates real estate openings.

Takeaway: You don’t need to predict 2026—you just need the right signals to know when to buy, refinance, or reposition for long-term growth.

If you want help running the numbers on buying, refinancing, or restructuring in 2026, message me “FRAMEWORK” and I’ll walk you through this 4-part model for your exact situation.