Falling in love with a home before running the numbers is how many first-time buyers turn a dream into stress. The house doesn’t break the budget — the payment does.

#1 Payment Comfort Beats Purchase Price

Most buyers ask, “How much can I get approved for?” when the smarter question is, “How much can I comfortably afford every month?”

Take a real example:

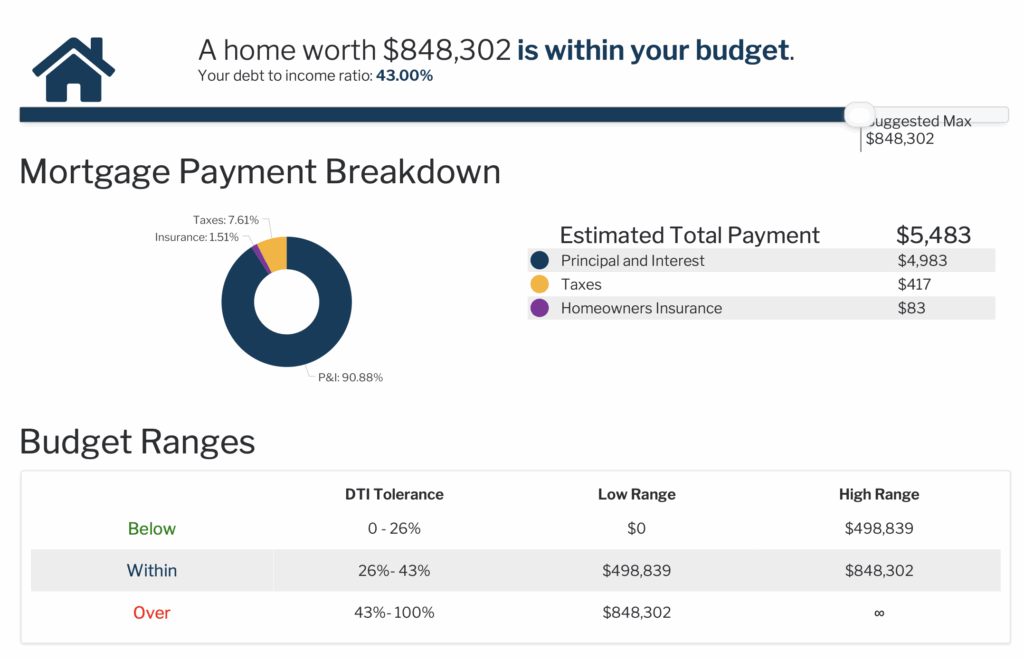

A buyer earning $160,000 annually with minimal monthly debt can technically qualify for a home around $848,000. On paper, that looks like success.

But here’s the reality: that home comes with a $5,483 monthly payment — $4,983 in principal and interest, plus $417 in taxes and $83 for insurance — pushing their debt-to-income ratio to 43%, right at the upper edge of comfort.

Visual Snapshot: What “Within Budget” Really Looks Like

A buyer earning $160K per year may qualify for an $848K home, but at a $5,483 payment and 43% DTI, that’s the financial edge — not breathing room.

That visual tells the story instantly: being “approved” doesn’t mean being “comfortable.”

I’ve seen clients choose to scale down from this upper limit and free up $400–$800 a month — giving them breathing room for savings, travel, and the unpredictable parts of life.

Owning a home you can live in comfortably will always beat owning one you can barely afford.

#2 The “Silent Costs” That Sneak Up

Homeownership isn’t just a mortgage. It’s taxes, insurance, maintenance, utilities, and the random water heater that quits mid-winter.

These aren’t extras — they’re the hidden layers of true affordability. Buyers who overlook them often find themselves stretched by month three.

A good rule: expect 1–2% of your home’s value in annual upkeep. That’s $8,000–$16,000 per year on an $800K home. It sounds steep, but planning for it keeps your finances (and sanity) intact.

Ignoring hidden costs doesn’t make them disappear. It just makes them harder to pay for.

#3 Stop Obsessing Over the Rate

Rates are temporary. Regret lasts longer.

Many buyers fixate on getting the lowest possible interest rate and miss the bigger picture.

I’ve seen clients delay purchasing for months waiting for a 0.25% drop — only to watch home prices climb by tens of thousands in the meantime.

Focus on strategy, not timing.

Use tools like rate locks, temporary buydowns, and refinance options to manage costs over time. What matters isn’t today’s rate — it’s whether your overall plan makes sense for your goals.

The smartest buyers focus on the plan, not the headline rate.

Takeaway:

The smartest move isn’t finding the cheapest mortgage — it’s finding the most sustainable one.

Buy the home that fits your life today and your goals tomorrow.

Because in the end, the best home isn’t the one that stretches your budget — it’s the one that supports your peace of mind.